Limitation period for transport tax for individuals

Car owners who have old transport tax debts should keep in mind that there is a limitation period for this type of payment. This means that the tax authorities not always entitled demand the repayment of such debts.

This review material will help you understand what the statute of limitations is for bringing to responsibility for non-payment of tax and how it differs from the statute of limitations, as well as when a citizen may no longer pay anything to the state.

The limitation period for bringing to responsibility for non-payment of transport tax

All time intervals during which are established at the legislative level. In 2019, the limitation period for transport tax for violations of its payment is regulated h. 1 tbsp. 113 of the Tax Code... According to it, if from the next day after the end of the tax period or from the date of the violation of the payment of taxes passed 3 years, then the person who committed the tax violation cannot be held liable.

Abs. 1 h. 1 tbsp. 113 of the Tax Code

A person cannot be held liable for a tax offense if three years have elapsed since the day it was committed or from the next day after the end of the tax (settlement) period during which this offense was committed and before the decision to prosecute was made ( limitation period).

Thus, the statute of limitations for tax evasion is 3 years. In case of non-payment of transport tax, legal entity a person, a three-year period is counted from the next day after the end of the tax period, that is, the year for which no tax has been paid.

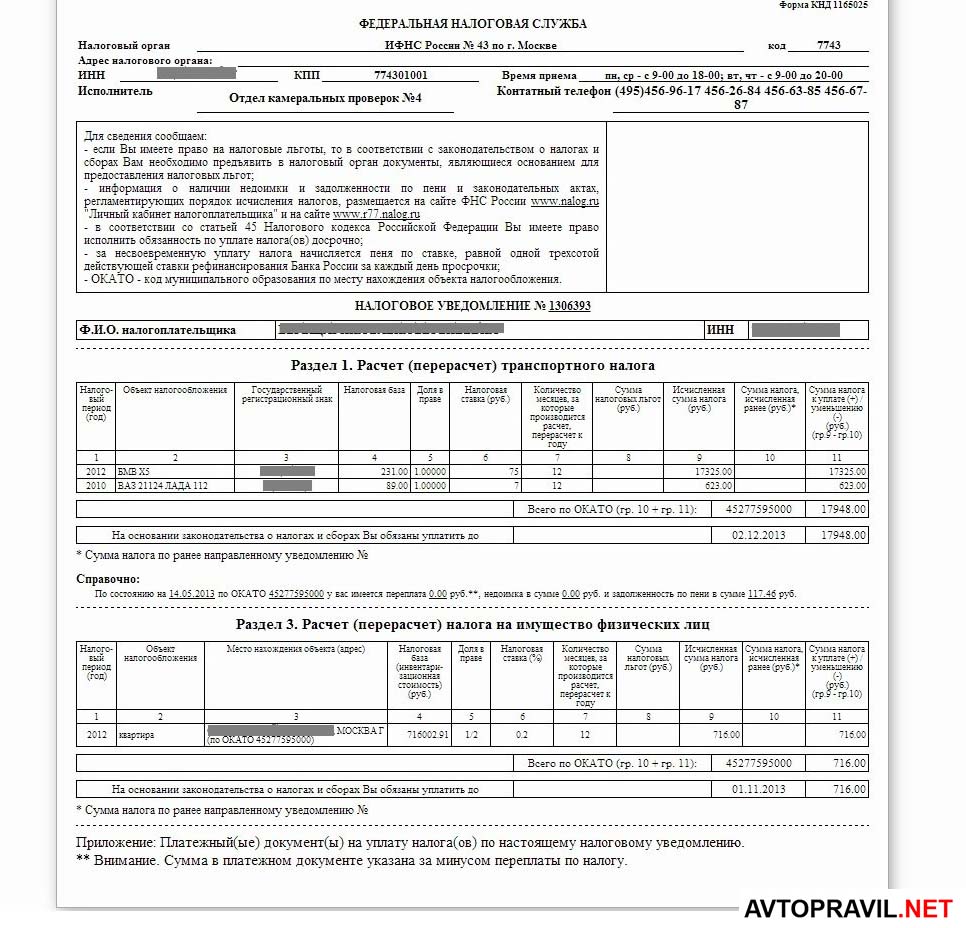

Individuals, unlike organizations, do not calculate the tax amount on their own, the Federal Tax Service does it for them, sending the results of the calculations in a tax notification. According to clause 3 of Art. 363 of the Tax Code of the Russian Federation the notice cannot indicate the amount of tax for more than 3 years preceding the current one. And physical. the person, in turn, does not have to pay debts that were incurred for tax periods earlier than these 3 years.

Item 3, Art. 363 of the Tax Code of the Russian Federation

Sending a tax notice is allowed for no more than three tax periods preceding the calendar year of sending it.

The taxpayers referred to in the first paragraph of this clause shall pay tax for no more than three tax periods preceding the calendar year of sending the tax notification specified in the second paragraph of this clause.

This means that the tax notice you receive in 2019 may only show the amount owed for the previous 3 years and pay taxes assessed earlier than this period, you should not.

What is the statute of limitations and when does it expire?

Do not confuse the statute of limitations for bringing to responsibility for tax offenses, which we talked about above, and the statute of limitations. The limitation period is the period during which FTS has the right to go to court to collect tax arrears from the debtor.

To nat. persons paid taxes on time and did not accumulate arrears, the tax office takes the following steps:

If the taxpayer has not paid the debt after receiving the claim, the tax authority has the right to sue him, and it is obliged to do this within a certain time frame. Limitation period for transport tax depends on the date of receipt claims for payment of debt and its total amount. At the end of this period, the tax authority loses the right to demand payment of the debt. The general limitation period is three years. Unless otherwise provided by law, the course of the limitation period begins on the day when the person found out or should have found out about the violation of his right and about who is the proper defendant in the claim for the protection of this right ( Articles 196, 200 of the Code of Civil Procedure of the Russian Federation).

Let's take a closer look at each stage.